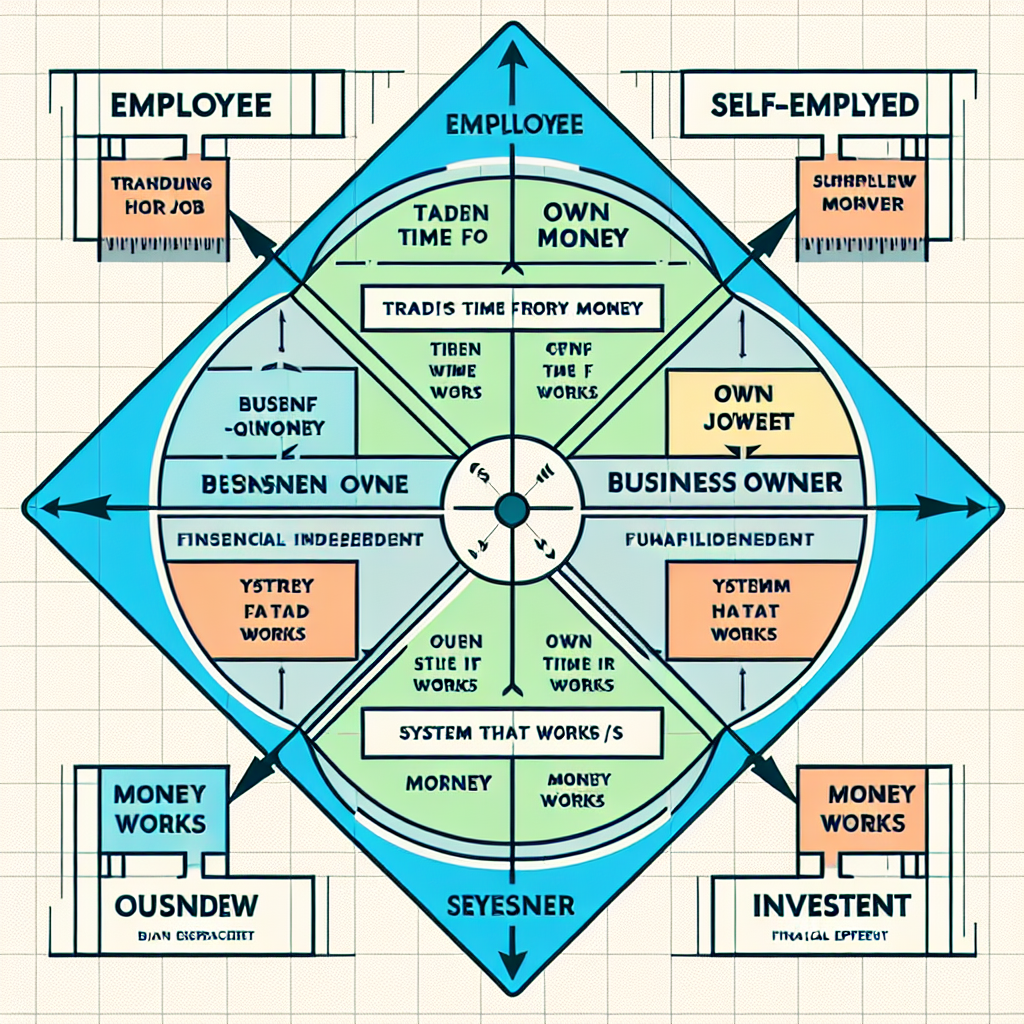

Robert Kiyosaki’s Cashflow Quadrant Explained: How to Achieve Financial Independence

Understanding The Four Quadrants: Employee, Self-Employed, Business Owner, And Investor

Robert Kiyosaki’s Cashflow Quadrant is a powerful framework that helps individuals understand the different ways people earn income and how these methods impact their journey toward financial independence. The quadrant is divided into four sections: Employee, Self-Employed, Business Owner, and Investor. Each quadrant represents a distinct approach to generating income, and understanding these can be crucial for anyone looking to achieve financial freedom.

Starting with the Employee quadrant, this is where most people begin their financial journey. Employees trade their time for money, working for someone else in exchange for a paycheck. While this provides a sense of security and stability, it also means that their earning potential is limited by the number of hours they can work. Additionally, employees often face the highest tax burdens, which can further limit their ability to accumulate wealth. Despite these limitations, being an employee can offer valuable experience and skills that can be leveraged in other quadrants.

Transitioning to the Self-Employed quadrant, individuals in this category work for themselves. They might be freelancers, consultants, or small business owners. While self-employed individuals have more control over their work and income, they also bear the full responsibility for their business’s success or failure. This can mean longer hours and more stress, but it also offers the potential for higher earnings compared to being an employee. However, like employees, self-employed individuals often find that their income is still tied to the amount of time they can dedicate to their work.

Moving on to the Business Owner quadrant, this is where the real shift in mindset occurs. Business owners build systems and hire people to work for them, allowing them to generate income without being directly involved in the day-to-day operations. This creates a scalable model where the business can grow and generate revenue independently of the owner’s time. Business owners benefit from leveraging other people’s time and skills, which can lead to significant financial gains. Additionally, they often enjoy more favorable tax treatment compared to employees and self-employed individuals. However, building a successful business requires a different set of skills, including leadership, strategic planning, and risk management.

Finally, the Investor quadrant represents the pinnacle of financial independence. Investors put their money to work for them by acquiring assets that generate passive income, such as stocks, real estate, or businesses. This allows them to earn money without actively working, providing the ultimate form of financial freedom. Investors benefit from the power of compounding returns and can achieve substantial wealth over time. However, becoming a successful investor requires knowledge, patience, and a willingness to take calculated risks.

Understanding these four quadrants is essential for anyone looking to achieve financial independence. By recognizing where they currently stand and where they want to go, individuals can make informed decisions about their career and financial strategies. Transitioning from one quadrant to another often involves acquiring new skills, changing mindsets, and taking on new challenges. However, the rewards of financial independence make this journey worthwhile.

In conclusion, Robert Kiyosaki’s Cashflow Quadrant provides a valuable roadmap for achieving financial independence. By understanding the differences between being an employee, self-employed, a business owner, and an investor, individuals can chart a course that aligns with their financial goals and aspirations. Whether you are just starting your career or looking to make a change, the Cashflow Quadrant offers insights that can help you navigate the path to financial freedom.

Transitioning From Employee To Business Owner: Steps To Financial Freedom

Transitioning from being an employee to becoming a business owner is a significant step towards achieving financial independence, and Robert Kiyosaki’s Cashflow Quadrant offers a clear roadmap for this journey. The Cashflow Quadrant, a concept introduced in Kiyosaki’s book ”Rich Dad’s Cashflow Quadrant,” categorizes the different ways people earn income into four distinct groups: Employee (E), Self-Employed (S), Business Owner (B), and Investor (I). Understanding these quadrants and how to move from one to another is crucial for anyone aspiring to financial freedom.

Initially, most people start in the Employee quadrant, where they trade time for money, working for someone else and earning a steady paycheck. While this provides financial stability, it often limits the potential for significant wealth accumulation. To transition from being an employee to a business owner, one must first shift their mindset. This involves recognizing that true financial independence comes from generating passive income, which is income earned with minimal effort on your part.

The first step in this transition is to develop a clear vision of your financial goals and the lifestyle you desire. This vision will serve as your motivation and guide throughout the journey. Next, it’s essential to acquire the necessary knowledge and skills. This can be achieved through education, whether formal or self-taught, and by seeking mentorship from successful business owners. Learning about business management, marketing, and financial planning will equip you with the tools needed to run a successful enterprise.

Once you have a solid foundation of knowledge, the next step is to identify a viable business opportunity. This could be based on your passions, skills, or market demand. Conduct thorough market research to ensure there is a need for your product or service and that you can offer something unique. Developing a comprehensive business plan is crucial at this stage, as it will outline your business strategy, target market, financial projections, and operational plan.

Securing funding is often a significant hurdle for aspiring business owners. Depending on your business model, you may need to explore various financing options such as personal savings, loans, or investors. It’s important to have a clear understanding of your financial needs and to create a budget that will sustain your business through its initial stages.

As you transition into the Business Owner quadrant, it’s vital to build a strong team. Surround yourself with individuals who complement your skills and share your vision. Delegating tasks and responsibilities will allow you to focus on strategic planning and growth. Additionally, investing in technology and systems that streamline operations can enhance efficiency and scalability.

Throughout this journey, maintaining a growth mindset is essential. Embrace challenges as learning opportunities and be willing to adapt to changing circumstances. Networking with other business owners and joining professional organizations can provide valuable support and insights.

Finally, as your business grows and becomes more profitable, consider transitioning into the Investor quadrant. This involves using your business profits to invest in other ventures, real estate, or the stock market, thereby creating multiple streams of passive income. By diversifying your investments, you can further secure your financial future and achieve true financial independence.

In conclusion, transitioning from an employee to a business owner requires a combination of vision, education, planning, and perseverance. By following the steps outlined in Robert Kiyosaki’s Cashflow Quadrant, you can navigate this journey successfully and move closer to achieving financial freedom.

The Importance Of Mindset In Moving From Self-Employed To Investor

Robert Kiyosaki’s Cashflow Quadrant Explained: How to Achieve Financial Independence

The journey from being self-employed to becoming an investor is not merely a change in how one earns money; it is a profound shift in mindset. Robert Kiyosaki, in his book ”Cashflow Quadrant,” emphasizes the importance of understanding the different ways people generate income and how transitioning from one quadrant to another can lead to financial independence. The Cashflow Quadrant is divided into four sections: Employee (E), Self-Employed (S), Business Owner (B), and Investor (I). Each quadrant represents a different approach to work and income, and moving from the S quadrant to the I quadrant requires a significant transformation in how one thinks about money, risk, and opportunity.

Initially, many people find themselves in the Self-Employed quadrant, where they trade their time for money. While being self-employed offers more control and flexibility compared to being an employee, it often comes with its own set of challenges. Self-employed individuals typically work long hours and are heavily reliant on their own efforts to generate income. This can lead to a situation where their financial well-being is directly tied to their ability to work, making it difficult to achieve true financial freedom. To move from being self-employed to becoming an investor, one must first adopt a mindset that values passive income over active income.

One of the key mindset shifts required is understanding the concept of leverage. In the Self-Employed quadrant, individuals often rely solely on their own skills and efforts. However, in the Investor quadrant, the focus shifts to leveraging other people’s time, money, and expertise to generate income. This means learning to identify and invest in opportunities that can provide returns without requiring constant personal involvement. For instance, investing in real estate, stocks, or businesses can create streams of passive income that continue to flow even when one is not actively working.

Another crucial aspect of this mindset shift is developing a tolerance for risk. Self-employed individuals may be accustomed to a certain level of control and predictability in their work. However, investing often involves a higher degree of uncertainty and requires a willingness to take calculated risks. This does not mean being reckless, but rather, being informed and strategic about where and how to invest. Educating oneself about different investment options, understanding market trends, and learning from successful investors can help build the confidence needed to navigate the world of investing.

Moreover, moving from self-employed to investor also involves cultivating a long-term perspective. While self-employed individuals might focus on immediate income and short-term goals, investors think in terms of years or even decades. This long-term outlook allows investors to weather market fluctuations and stay committed to their investment strategies. It also encourages the practice of reinvesting earnings to compound wealth over time, rather than spending it all on immediate needs or desires.

In addition to these mindset shifts, it is essential to build a strong financial foundation. This includes managing personal finances effectively, reducing debt, and saving a portion of income for investment purposes. Having a solid financial base provides the security and resources needed to take advantage of investment opportunities as they arise.

In conclusion, transitioning from being self-employed to becoming an investor is a journey that requires a significant change in mindset. By embracing the principles of leverage, risk tolerance, long-term thinking, and financial discipline, individuals can move towards the Investor quadrant and achieve financial independence. Robert Kiyosaki’s Cashflow Quadrant serves as a valuable guide in this process, offering insights and strategies to help individuals transform their approach to earning and managing money.

Strategies For Building A Successful Business In The Cashflow Quadrant

Robert Kiyosaki’s Cashflow Quadrant Explained: How to Achieve Financial Independence

In the pursuit of financial independence, understanding Robert Kiyosaki’s Cashflow Quadrant can be a game-changer. The Cashflow Quadrant, introduced in Kiyosaki’s book ”Rich Dad’s Cashflow Quadrant,” categorizes the different ways people earn income into four distinct groups: Employee (E), Self-Employed (S), Business Owner (B), and Investor (I). Each quadrant represents a different approach to generating income, and transitioning from one quadrant to another can significantly impact your financial future. To build a successful business within the Cashflow Quadrant, it is essential to adopt specific strategies that align with the principles of the B and I quadrants.

First and foremost, shifting from the E or S quadrant to the B quadrant requires a change in mindset. Employees and self-employed individuals often trade time for money, whereas business owners leverage systems and people to generate income. To make this transition, it is crucial to develop a vision for your business that goes beyond your personal efforts. This means creating scalable systems and processes that can operate independently of your direct involvement. For instance, investing in technology that automates routine tasks or hiring skilled employees who can manage different aspects of the business can free up your time to focus on strategic growth.

Moreover, building a successful business in the B quadrant necessitates a strong emphasis on leadership and team-building. Unlike the S quadrant, where you might be the sole operator, the B quadrant thrives on collaboration and delegation. Effective leaders inspire and motivate their teams, fostering a culture of innovation and accountability. By empowering your employees and providing them with the tools and resources they need to succeed, you create a robust foundation for your business. Additionally, continuous learning and development are vital. Staying updated with industry trends and investing in professional development for yourself and your team can keep your business competitive and adaptable.

Another critical strategy is financial literacy. Understanding the financial aspects of running a business, such as cash flow management, budgeting, and financial forecasting, is indispensable. This knowledge enables you to make informed decisions that can drive your business forward. For example, maintaining a healthy cash flow ensures that your business can weather economic downturns and seize growth opportunities. Furthermore, having a clear financial plan helps you set realistic goals and measure your progress, providing a roadmap for sustainable success.

Transitioning to the I quadrant, where your money works for you, involves strategic investments that generate passive income. As a business owner, reinvesting profits into assets such as real estate, stocks, or other businesses can diversify your income streams and build long-term wealth. It is essential to conduct thorough research and seek advice from financial experts to make prudent investment choices. Additionally, understanding the power of compounding and the importance of starting early can significantly enhance your investment returns over time.

Networking and mentorship also play a pivotal role in building a successful business within the Cashflow Quadrant. Surrounding yourself with like-minded individuals and learning from experienced mentors can provide valuable insights and guidance. Networking opportunities, such as industry conferences and business associations, can open doors to potential partnerships and collaborations that can propel your business to new heights.

In conclusion, achieving financial independence through the Cashflow Quadrant requires a strategic approach to building a successful business. By adopting a scalable mindset, emphasizing leadership and team-building, enhancing financial literacy, making strategic investments, and leveraging networking and mentorship, you can transition from the E or S quadrant to the B and I quadrants. These strategies not only pave the way for business success but also set the foundation for long-term financial freedom.

How To Create Passive Income Streams As An Investor For Long-Term Wealth

Creating passive income streams as an investor is a crucial step toward achieving long-term wealth and financial independence. Robert Kiyosaki, the renowned author of ”Rich Dad Poor Dad,” offers valuable insights into this process through his Cashflow Quadrant. This quadrant categorizes the different ways people earn money into four distinct sections: Employee (E), Self-Employed (S), Business Owner (B), and Investor (I). Understanding these categories and transitioning from the left side of the quadrant (E and S) to the right side (B and I) can significantly enhance your financial prospects.

To begin with, the Employee and Self-Employed categories represent active income, where you trade time for money. While these roles are essential, they often limit your financial growth due to the finite nature of time. On the other hand, the Business Owner and Investor categories focus on generating passive income, where money works for you. This shift is fundamental for building long-term wealth and achieving financial independence.

As an investor, creating passive income streams involves strategically allocating your resources into various investment vehicles. One of the most popular methods is investing in real estate. Rental properties, for instance, can provide a steady stream of income while appreciating in value over time. By carefully selecting properties in high-demand areas and maintaining them well, you can ensure a reliable income source. Additionally, real estate investment trusts (REITs) offer a more hands-off approach, allowing you to invest in real estate without the responsibilities of property management.

Another effective way to generate passive income is through dividend-paying stocks. By investing in companies with a history of consistent dividend payments, you can receive regular income without selling your shares. This strategy not only provides cash flow but also allows your investment to grow through capital appreciation. Moreover, reinvesting dividends can compound your returns, further accelerating your wealth-building journey.

Peer-to-peer lending platforms also present an opportunity to earn passive income. By lending money to individuals or small businesses through these platforms, you can receive interest payments over time. While this method carries some risk, diversifying your loans across multiple borrowers can mitigate potential losses and enhance your overall returns.

Furthermore, creating and selling digital products can be a lucrative passive income stream. E-books, online courses, and software applications are examples of digital products that can generate income long after their initial creation. By leveraging your expertise and marketing these products effectively, you can build a sustainable income source that requires minimal ongoing effort.

Investing in index funds and exchange-traded funds (ETFs) is another strategy to consider. These funds offer broad market exposure and typically have lower fees compared to actively managed funds. By investing in a diversified portfolio of index funds or ETFs, you can achieve steady returns with reduced risk, making them an attractive option for long-term wealth building.

In addition to these methods, it’s essential to continuously educate yourself and stay informed about market trends and investment opportunities. Attending seminars, reading books, and following financial news can help you make informed decisions and adapt your strategies as needed.

In conclusion, transitioning to the Investor quadrant and creating passive income streams is a powerful way to achieve financial independence and long-term wealth. By exploring various investment options such as real estate, dividend-paying stocks, peer-to-peer lending, digital products, and index funds, you can build a diversified portfolio that generates consistent income. With dedication, education, and strategic planning, you can harness the power of passive income to secure your financial future.